.avif)

.avif)

Get a guide to creating pitch decks presentation

.avif)

.png)

Most SaaS founders rebuild a deck the way they would touch up a website: drop new logos onto the cover, update the ARR number, freshen the AI line, ship. The deck that closed the previous round becomes the template for the next one. The problem is that the people on the other side of the table are not the same. According to DocSend's 2024 Pitch Deck Metrics, investors now spend about 2 minutes 30 seconds on a deck before deciding whether to keep reading, and the questions the 2020-2022 investor cohort opened with look fundamentally different from the questions the 2024-2026 cohort opens with. The updated-numbers deck quietly fails. This article is a practitioner read of what changed and what three real decks did about it, drawing on Whitepage Studio's pitch deck design methodology. A working definition first.

A SaaS investor pitch deck is a 10 to 15 slide argument for why an investor should fund the company at the round being raised. The slide set is largely what founders were assembling in 2018. The argument is not. The rest of this article shows what it looks like now: what investors read first, how three real decks held up, what shifted between 2022 and 2026, and how the spine changes between Series A and Series B.

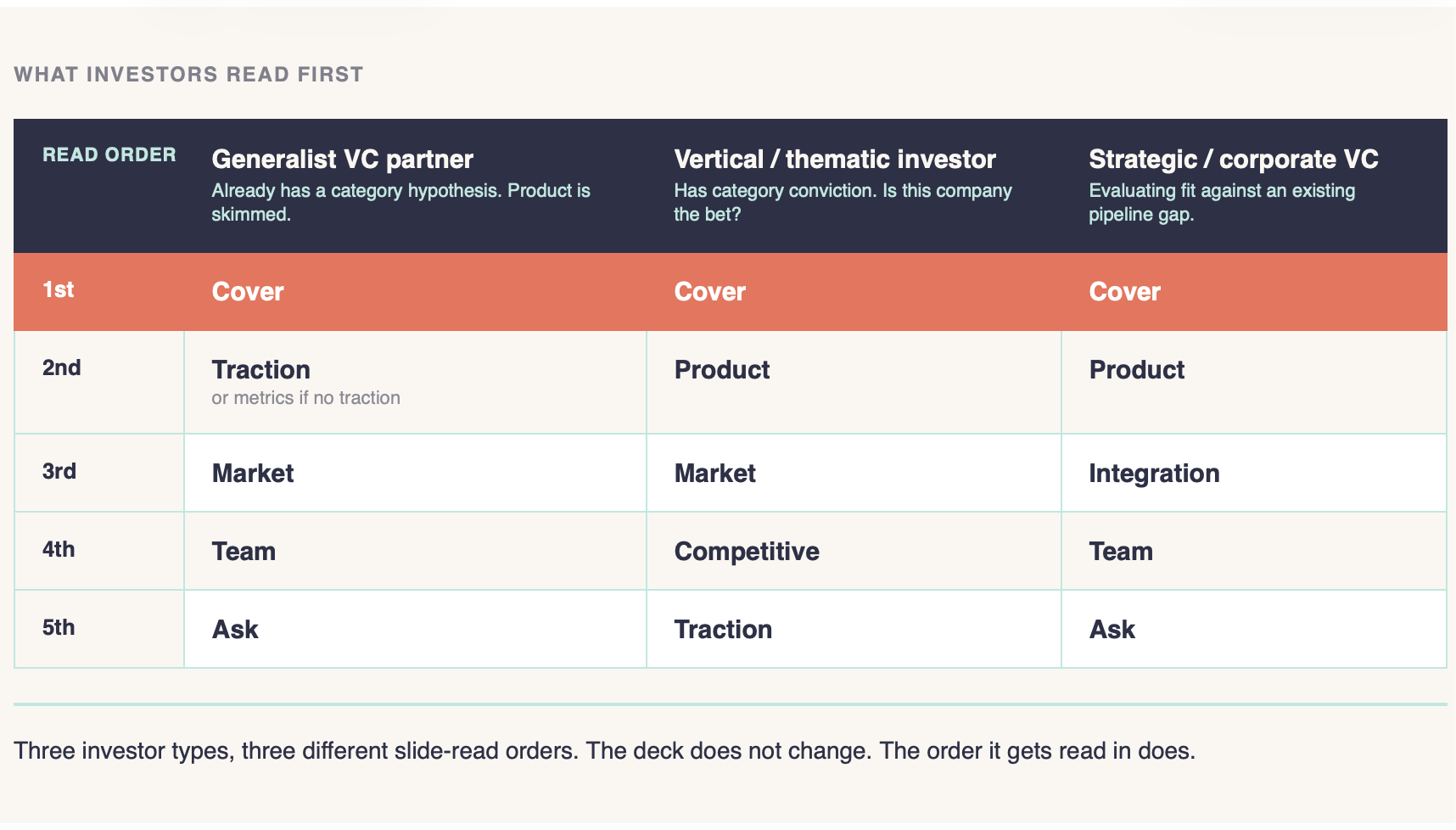

The order an investor reads slides matters more than which slides are in the deck. Three observable reading patterns recur across the post-2024 cohort, depending on the type of investor opening the file.

Generalist VC partner - reads cover, then traction (or metrics if there is no traction), market, team, ask. Product is skimmed; the partner already has a category hypothesis.

Vertical / thematic investor - reads cover, then product, market, competitive, traction. They have category conviction; the question is whether this company is the bet.

Strategic / corporate VC - reads cover, then product, integration / partnership angle, team, ask. They are evaluating fit against an existing pipeline gap.

With sub-three-minute average review time (DocSend), the partner is not reading the deck the way the founder wrote it. They are scanning to confirm or reject a hypothesis they brought into the meeting. The generalist is checking whether this company fits a category they already underwrite. The vertical investor has the category conviction and is asking whether this is the right bet inside it. The strategic VC is matching the product against a pipeline gap; the integration slide does the work the traction slide does for a generalist.

These are observable patterns, not laws. Design the deck against the most likely reading order for the cohort.

The practitioner takeaway sits on the cover. The cover is the only slide guaranteed to be read, and most SaaS founders waste it on a logo and a tagline. The strongest cover slides state the defining metric or contradiction. Front framed shared inboxes as a coordination problem. Pendo positioned analytics as upstream input to product decisions, not downstream reporting. Airbyte claimed open-source community traction as a leading indicator of category creation. All three earned the next sixty seconds, which, given the DocSend number, is most of the meeting.

Of the three patterns, the strategic-VC one is the most underestimated. The Front teardown opens at the integration slide for that reason.

A working set of calibrations we apply when auditing a SaaS pitch deck design.

The single highest-leverage calibration is the cover slide. The three decks in the next section each made a cover-slide move worth borrowing.

What the three decks below share: each won its round by reframing what the deck was arguing, not by adding slides. Same canonical SaaS spine - cover, problem, solution, market, traction, team, ask. Different argument loaded onto it.

Front raised $10 million in 2016 with a deck that did one thing: it reframed the category. The product description on the surface was "team email." The deck moved it to "customer-facing communication platform," and that reframe carried the slides.

The signature move is on the problem slide. Front did not pitch a broken inbox; it pitched coordination cost. Once shared inboxes were the coordination problem, the solution slide didn't have to argue that team email was a category. It could argue that Front was the platform for a category investors were already willing to fund (customer operations infrastructure).

The proof slides did the rest. Early-customer logos demonstrated PMF in the operations-heavy segment Front had bet on. Expansion revenue showed seats expanded inside an account once one team adopted Front. Vertical penetration on a small set of customer types made the case for a deliberate wedge.

The integration slide is the one strategic investors open the deck to. Front's showed the existing tools it sat alongside (Salesforce, Asana, the customer's helpdesk) rather than the tools it replaced. That made the deck readable to corporate VCs whose evaluation question is "does this fit our stack" rather than "does this disrupt the stack." Front built it as a first-class slide.

What the Front deck teaches: a category reframe at the problem slide gives every downstream slide a clearer job. The same principle is the spine of storytelling in a pitch deck - the structural choice at the top decides how much work the slides below have to do.

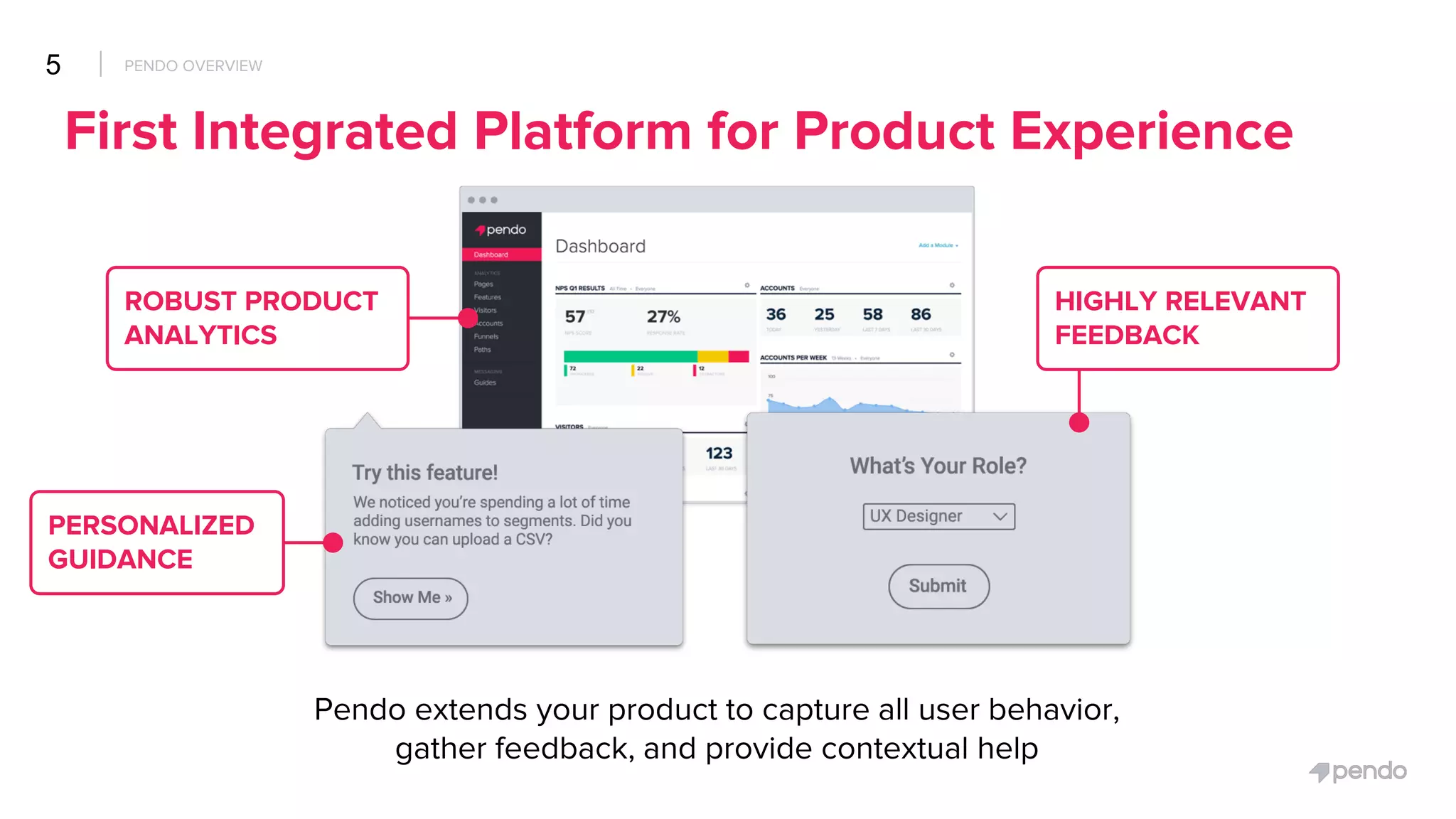

If Front's deck made a category-reframe argument, Pendo's made a positioning argument. Pendo raised $20 million in 2016 against the question that haunts every analytics startup: is this a feature or a company? The product slide answered it.

Pendo positioned itself as upstream input to product-market-fit decisions, not downstream BI reporting. The two are funded differently. Downstream BI is a tools market: competitive, margin-compressed, crowded. Upstream PMF input is product infrastructure: smaller market, higher conviction, with budgets from product engineering. By the time the investor got to the market slide, the question had moved from "how big is the BI market" to "how big is the product-infrastructure market" - and the second justifies a $20M round.

The product slide carried that positioning visually. Instead of leading with a dashboard (the cliche analytics screenshot), Pendo led with a screenshot of the product asking a user a question inside an app. The upstream-input argument in one frame.

What the Pendo deck teaches: when the category is crowded, the deck's job is positioning, not differentiation. Pendo did not argue better analytics; it argued a different kind of analytics, used by a different team, against a different decision. For a SaaS investor presentation in a competitive category, that move is almost always available and almost always under-used.

Front reframed a category. Pendo positioned inside one. Airbyte argued one was being created.

Airbyte raised $150 million in 2021 on a deck built around community-traction metrics as proof of category creation. The open-source thesis is the part most competing SaaS pitch articles do not address, and it is SaaS-specific: at this stage, GitHub stars, contributor counts, and deployment density predict enterprise demand at higher fidelity than a direct-sales pipeline.

The structural choice that made the deck work was treating community as the funnel. A traditional B2B SaaS pitch deck shows pipeline: SQLs, opportunities, closed-won. Airbyte's showed contributors and deployments, then showed conversion from community user to paying enterprise customer already had a slope. Investors with open-source theses had a framework for those numbers. Investors who did not, did not write the check.

The category-creation argument carried the ask. A $150M Series B on a relatively early commercial product is hard to justify on revenue alone, but easier on the basis that the company is the default infrastructure for a category that did not exist three years earlier. Airbyte did not pitch a faster ETL tool. It pitched the platform for a category.

What the Airbyte deck teaches: open-source-led SaaS has a different deck spine than direct-sales SaaS. The traction slides come earlier, customer logos matter less, and community metrics carry weight a sales-led deck does not have. If running an OSS-led GTM, do not borrow the sales-led template.

The three moves above are not interchangeable. The right one depends on where the deck sits in its market.

The three decks worked because the deck reading frame in 2016-2021 still rewarded category-level argument. The next section is about what shifted in that frame.

The 2022 SaaS deck template is now a liability, for three specific reasons. The shifts below are observable across the 2024-2026 cohort in our practice.

Rebuilding the deck against the current reading frame is the highest-leverage update most SaaS founders can make to a deck written before 2023. Not every SaaS category aged the same way - vertical and enterprise SaaS with long category dominance still close some rounds on growth-led decks. The template aged, not the category.

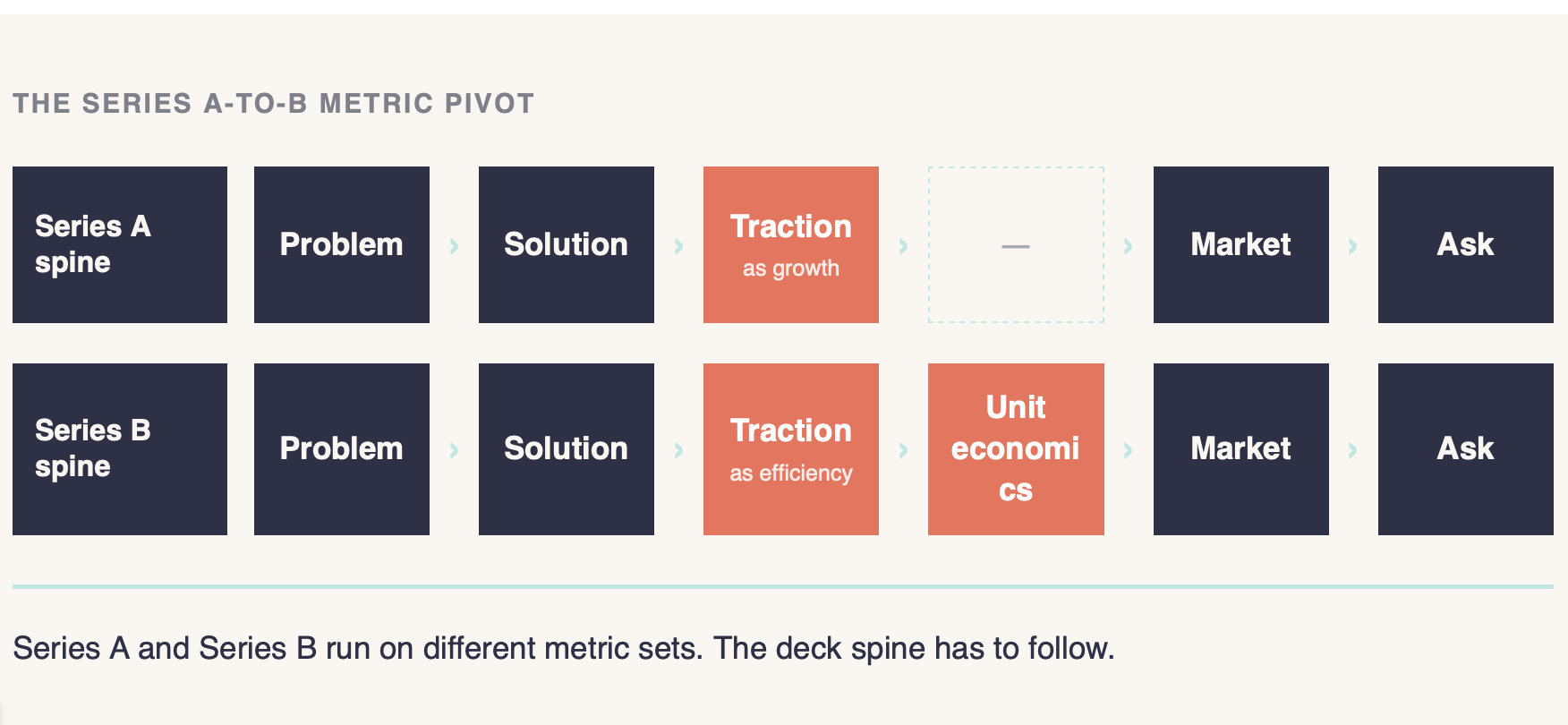

The most concrete example of the rebuild is the Series A-to-B pivot.

The three checks we run first when a founder hands us a deck that closed a previous round.

These three updates surface at the metric level, but they cascade into structure: the burn-multiple slide changes where retention sits, which changes the cover slide, which changes the meeting. The Series A-to-B pivot is the cleanest place to see that cascade.

Same product, same trajectory, different deck spine, because the question the round asks changes at the Series B inflection. ICONIQ's 2025 benchmark notes that NRR is "settling into a healthy ~110-120% range," which is now the implicit pass/fail line at the Series B retention slide.

Take a hypothetical SaaS company, call it Reframe. At Series A, the deck spine is: problem - solution - traction-as-growth - market - ask. The growth slide is the hero. Two years later, at Series B, the spine is: problem - solution - traction-as-efficiency - unit economics - market - ask. The growth curve still appears, but behind the efficiency slides. Same evidence, reordered. For the sequence holding across both spines, see the pitch deck narrative structure breakdown.

A calibration: "Series B always leads with NRR" is conditional. NRR leads when it is best-in-class for the category; otherwise gross margin or payback leads. The series b saas pitch deck spine is a reweighting, not a wholesale slide swap. Founders who hand a Series B investor the Series A deck with metrics updated miss the structural shift.

Book a complimentary consultation - we'll review the deck spine behind your current SaaS round.

The benchmarks we run when auditing the metric block of a Series A or Series B deck.

The metric pivot is the cleanest instance of the broader shift between 2022 and 2026. The mistakes below are the failure modes that show up when founders try to make the pivot without restructuring the deck.

These are the failure modes we still see across SaaS decks, with three now carrying a 2026-specific edge. Calibrated for self-check, not for drama.

The recurring failure mode across all seven: the deck is treated as a document instead of a sequence. The deck that gets read in order gets read at all.

Read also: Common Presentation Design Mistakes

Two checks worth running before the deck leaves the founder's laptop.

The mistakes above are surface symptoms. The structural answer is what the conclusion lands on.

A SaaS pitch deck in 2026 has to do three things the 2022 deck did not: explain the proprietary signal beneath the AI layer, show capital efficiency at the round, prove the product works across multiple customer cohorts. The three decks above - Front, Pendo, Airbyte - show three ways: a category reframe, a positioning move, a category-creation case. The wrong move would have been reusing a deck spine because it once worked.

One thing for the next deck rebuild: before touching slides, write the one sentence the deck has to prove for this round and this investor cohort. If the current cover slide does not state it, the deck is arguing the wrong thing.

The canonical SaaS spine is cover, problem, solution, market, business model, traction, team, ask - typically 10 to 15 slides. Which slides matter most depends on the investor (see "What investors read first" above) and the round (see "The Series A-to-B metric pivot" above). What changes between rounds is which slides carry the argument. For the canonical sequence, see Whitepage's pitch deck narrative structure breakdown.

10 to 15 slides is the working range at Seed and Series A. Series B decks tend toward the upper end because the unit-economics and retention slides take real estate earlier-stage decks do not need. The constraint is the sub-three-minute window of investor attention. More slides will not fix a deck that does not make its argument in that window. See Whitepage's pass on how many slides a pitch deck needs.

The spine is similar; the proof slides do different work. A general SaaS deck can lean on logo walls and self-serve conversion metrics. A b2b saas pitch deck for enterprise has to address sales cycle length, contract value, multi-stakeholder buying, and integration depth. The cover and ask are the same; traction and GTM change shape. Whitepage's pitch deck design work treats enterprise SaaS as a distinct engagement profile.

Three headline shifts, covered in the "What changed" section above: growth-at-all-costs gave way to capital efficiency, "AI-powered" as a tagline gave way to AI-native as a baseline, single-cohort proof gave way to multi-cohort proof. The 2026 deck addresses efficiency on the deck (not in the data room), articulates the proprietary signal beneath the AI layer, and shows evidence across multiple customer types. For the rebuilt spine, see Whitepage's pitch deck narrative structure breakdown.

Biotech and healthcare decks have to address regulatory pathway, clinical evidence, and reimbursement. SaaS decks typically do not. SaaS sits closer to the buyer; biotech and healthcare sit closer to a regulator. SaaS decks lead with traction and product; healthcare and biotech lead with science and pathway. For a worked example of the healthcare deck spine, see Whitepage's healthcare pitch deck examples.

867 BOYLSTON ST

BOSTON, MA 02116