.avif)

.avif)

.avif)

Get a guide to creating pitch decks presentation

.png)

.avif)

Investors decide whether to keep reading a pitch deck in under three minutes, and what they remember a week later is rarely the data. It is the shape of the story. A deck with no narrative spine blurs into every other deck in the stack, and the founders who raise are usually the ones who walked the partner through an argument, not a slide library. Storytelling in a pitch deck does the quiet work of making that argument legible when the deck is being read in silence on a Sunday afternoon.

Across 12 years and 4,000+ pitch decks, the slides Whitepage Studio most often hears investors recall back to founders are story slides, not market-size slides. The pitch deck design methodology we use rests on that pattern. This article walks four funded decks slide by slide, then makes two points the generic version misses.

TL;DR

Storytelling in a pitch deck supports a raise; it does not cause one. The strongest decks pair a narrative spine with stage-appropriate evidence and know when to compress one to make room for the other.

Pure-data decks blur together. The deck that gets remembered is the one with a narrative spine, the underlying argument that gives every slide a reason to be in that order.

The clearest public proof is Kabbage, the Atlanta fintech that raised more than $1.3 billion across its lifecycle and credited a story-first deck for its earliest meetings (Inc.). The data was always there. The data was not what got the rooms.

The evidence pillar is older than fundraising. Research from Motista found that customers who feel emotionally connected to a brand spend roughly twice what merely satisfied customers spend (PRNewswire). Investors are not customers, but the same wiring runs underneath. A story is what makes data stick.

Here is the calibrated frame the rest of this article rests on: storytelling in a pitch deck supports a raise; it does not cause one. The deck that closes pairs both, weighted for the round.

Before the prose, the model itself:

A startup's "unique story" is not what makes the company appealing in the abstract. It is the specific contradiction the company exists to resolve, the gap a reasonable person can see once it is named.

Airbnb's contradiction was "strangers in your home," a thing nobody in 2008 thought they would tolerate; the contradiction became the spine, and every later slide reframed the same tension. Buffer's proof of motion was radical transparency - publishing the deck publicly, publishing revenue, publishing salaries. The transparency itself was evidence the company could close the gap between social media tools that exist and a tool you can trust. LinkedIn's stake was the largest of the four: if professional networking moved online, every recruiting firm and every Rolodex was repriced overnight.

Contradiction, proof of motion, stake. Every other slide is structural support for those three. For a deeper breakdown of how the spine maps onto a slide sequence, see the pitch deck narrative structure reference.

The story does not have to be in the deck. It has to be in the founder's head when the deck is read in silence. The deck is the prop; the story is the script.

Generic pitch deck storytelling lists could come from any storytelling book. What matters is how each technique behaves inside a deck investors skim in minutes. Seven worth using:

The real question behind "balance data and story" is simpler than the phrasing suggests: how much data is too much. Rule of thumb - any data slide that is not load-bearing for the story should be cut, even when impressive. The deck is not a portfolio of the company's analytics; it is a single argument supported by the minimum evidence required to land that argument. The Facebook teardown below is the cleanest example of that discipline in practice.

The four decks below are widely studied and widely misread. Each is praised for "good storytelling." What is rarely shown is that each one used a different spine. Read in sequence, they make the case that the spine is dictated by the evidence configuration, not the founder's taste.

Spine: We do not need revenue to prove this works because the network effects are visible at every campus.

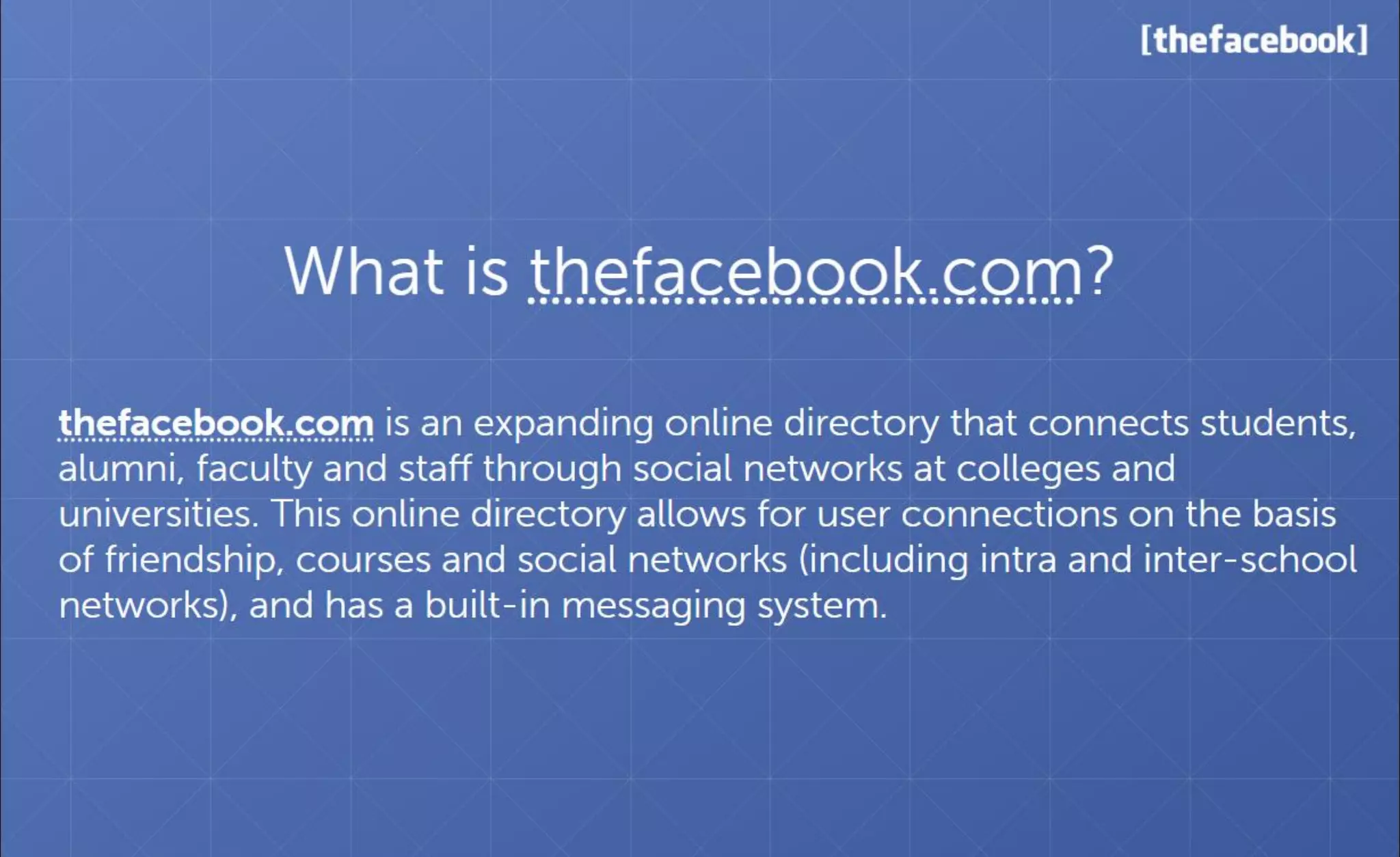

Facebook's 2004 deck had no revenue slide of consequence. It did not need one. What it had was a sequence of slides that compressed an unanswerable VC question - "how do you know this is real?" - into one verifiable number per campus.

The early-deck media kit Facebook circulated to advertisers (the de facto pitch deck) led with penetration metrics by school. Harvard adoption ran north of 70 to 80% in the first weeks. Stanford, Columbia, and Yale repeated the pattern within their own opening windows. The slides reported user counts, engagement rates, and college-by-college rollout - not revenue, not projections, not a forecast model. The argument is structural, not financial. The pattern is the proof.

Every metric is evidence for the same one-sentence claim: the network effect is replicating identically across distinct campuses, which means it is the network effect, not the campus. Strip the spine and the same numbers read as scattered traction across a handful of schools. Bolt the spine on and the same numbers become the underwriting case for a category.

For founders whose story rests on adoption data instead of revenue, the question is which numbers carry the argument and which are decoration. The metrics investors scrutinize at seed are not topline numbers; they are pattern numbers. That is a story argument with data backing, not a data argument with a story wrapper.

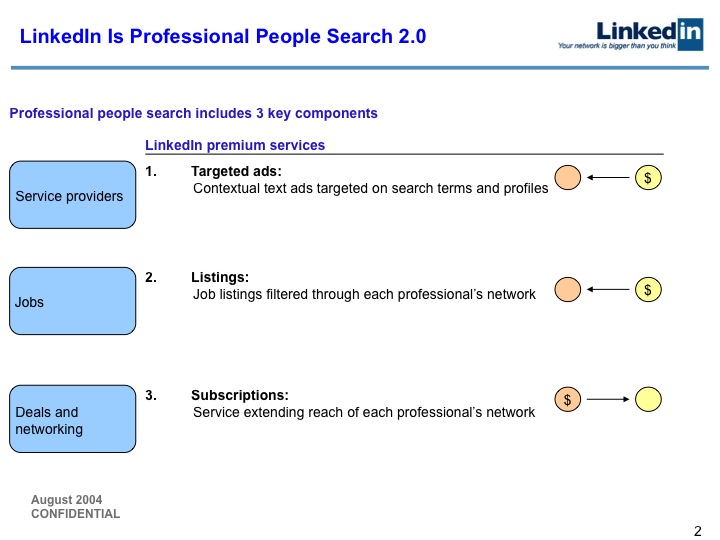

Spine: Professional networking is the next service to make the internet transition.

LinkedIn's Series B deck does something rare. It frames the company as the inevitable instance of a broader pattern - not the unique idea but the unique fit. The reframe lives on the "why now" slides. The deck walks through services that already moved offline to online (encyclopedias to Wikipedia, retail to Amazon, banking to PayPal) and places professional networking next in the queue. The slide does not argue that LinkedIn is special. It argues that the migration is happening, and that something will occupy the professional-networking slot whether the room invests or not.

This is category framing disguised as a why-now argument. Once the analogy lands, every later slide reads as inevitability evidence. The product slide is no longer "here is a clever new app"; it is "here is the implementation of the migration we already showed you." The traction slide becomes "here is the speed of the migration."

The mechanical move is the analogy chain. PayPal versus traditional banking is the closer of the chain because it is the most recent, most expensive, and most replicable migration in living investor memory. The investor does not have to leap on a new category. They have to agree the migration is happening and accept LinkedIn as its natural beneficiary.

When the analog markets are stronger than the company's own traction, lead with the analog chain. LinkedIn raised because the deck made professional networking feel pre-decided, not novel.

Spine: Repeat a three-element pattern across every slide so the deck feels like one continuous argument.

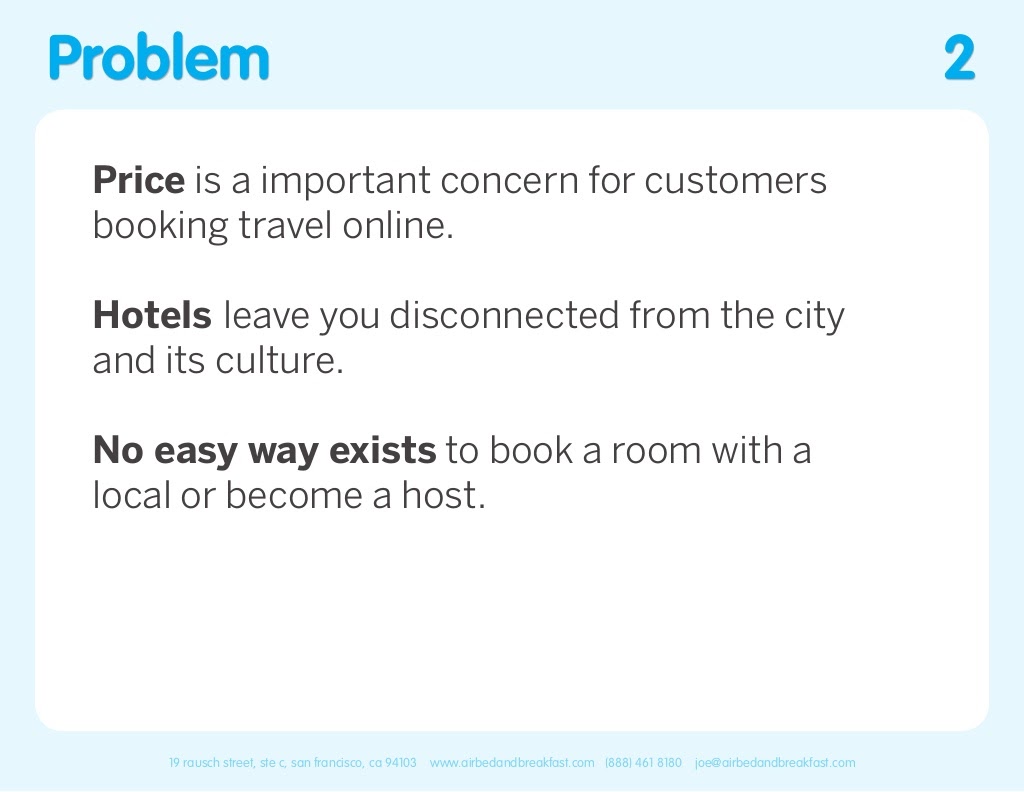

The Airbnb deck is the most rhythmically engineered pitch deck in the public funded-deck library. Every load-bearing slide is built in threes. The problem slide breaks the booking economy into three failures: price, inconvenience, and the absence of local culture. The solution slide answers with three counters: save money as a traveler, make money as a host, share a culture as both. The market slide stacks three quantifications: total trips booked, online trips, couch-surfing trips - each a successively narrower wedge that lands inside the Airbnb opportunity.

The repetition is not aesthetic. It is structural. Each three-element slide reframes the same contradiction - strangers in your home should not work, but here is why it does, here, here, and here. By the time the investor reaches the financials, they have absorbed the same argument seven different ways, and the rhythm itself signals discipline.

Even the language repeats. The problem slide and the solution slide use parallel sentence structures; the market slide uses parallel quantifications. An investor reading silently is not consciously aware of the rule of three; they are aware the deck feels coherent, that the slides argue rather than list. If a slide cannot be expressed as three parallel elements, it is doing two things at once and should be split. The rule of three is not a slide tactic. It is a discipline on the whole deck.

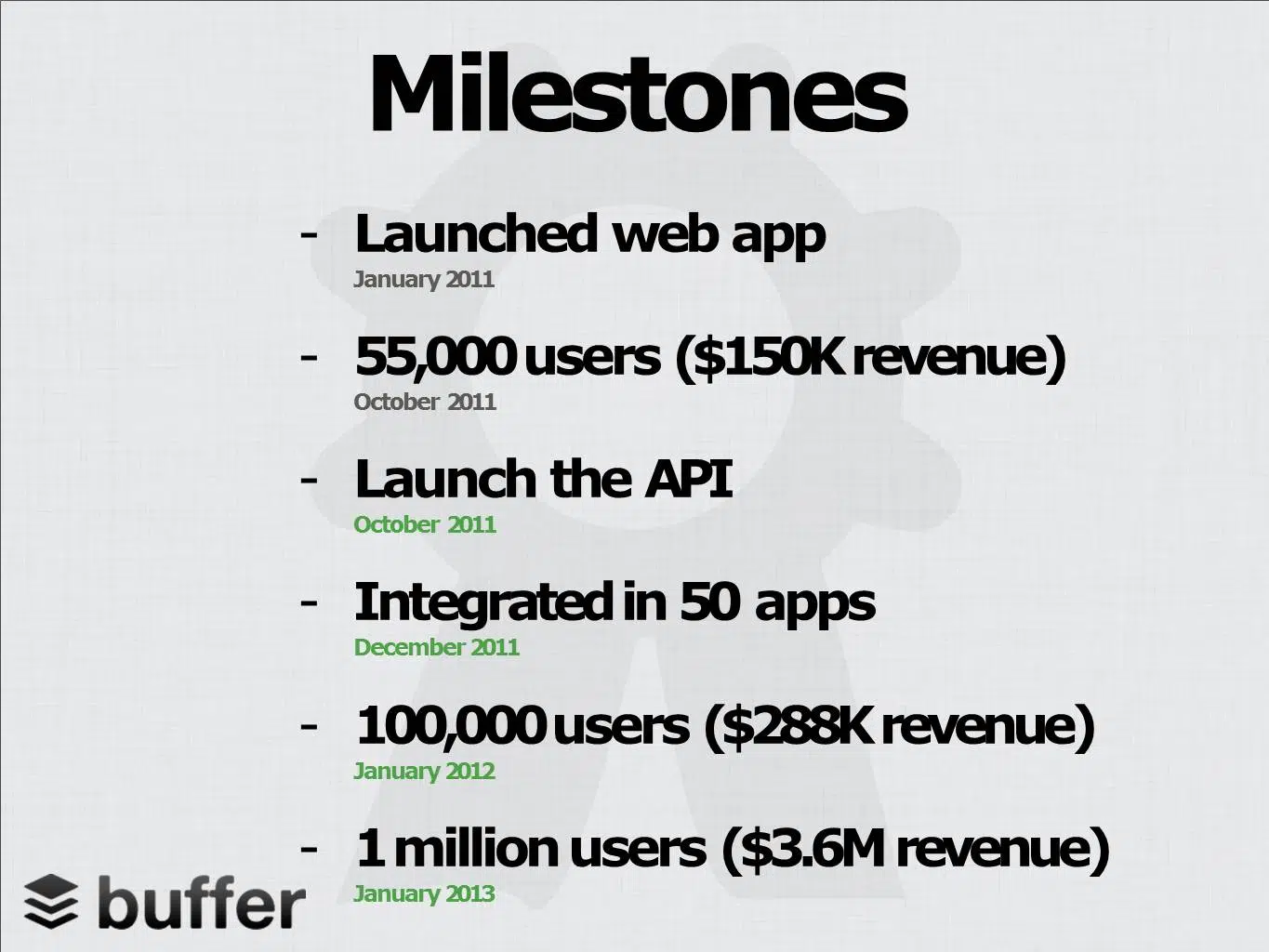

Spine: Buffer is the first company to publish its pitch deck publicly, and that act is the story.

Buffer's deck is the most contrarian of the four. It is not really about the product. It is about a company that operates differently from every other company in its category, publishing revenue, salaries, and internal metrics that everyone else treats as private. By making the deck public in 2013, Buffer turned a private investor document into the proof of motion for radical transparency. The MRR slide is not "here is our growth"; it is "here is what a transparent company looks like when it shows what most companies will not." Same numbers, different argument.

The metrics support the trust-and-transparency thesis. They do not lead it. App integrations, user counts, and annual revenue all appear on the deck, but each is framed as evidence that the operating choice is working - not as a market case to be litigated separately. The deck does not ask the investor to admire the numbers. It asks the investor to admire what kind of company produces those numbers in public.

Buffer's deck is the cleanest public example of a story spine that is not a hero's journey or a category reframe. It is a single operational choice - this is how we work - turned into the entire narrative. If the operational choice the company has made is the most distinctive thing about it, build the deck around that choice and let the numbers carry the consequence, not the headline.

This is one of the two reasons this article exists. The same fundraising round routes through three different narrative anchors depending on the vertical, and founders who borrow the wrong spine signal they do not yet know what their own evidence is.

Same Series A round, three different story spines. The biotech deck argues for a threshold the company has not yet crossed. The SaaS deck argues the threshold is already crossed. The consumer deck argues retention will hold without paid growth. Each spine is internally consistent only when it fits the evidence configuration in front of it. A founder who borrows the SaaS spine for a biotech deck signals to investors that the founder does not yet know what their own evidence is - and that misread is more common than people expect.

Here is the practitioner test. Take a single hypothetical product - an AI-driven clinical decision-support tool, one team, one codebase, one product roadmap - and route it three ways. Pitch it to a biotech VC and the spine is the clinical milestone: which conditions does the tool support, which sample sizes have been studied, which regulatory pathway is in motion, which readout date is next. Data is forecast: when does the evidence threshold arrive, and what does the deck look like the day after it does.

Pitch the same product to an enterprise SaaS investor and the spine reorders. The clinical evidence collapses into a footnote. The deployment story takes over: which hospital systems are signed, what is the average contract value, what is the implementation cycle, what is the velocity of net new logos quarter over quarter. Data is proof of the threshold crossing.

Pitch the same product to a consumer-health investor and the spine reorders again. Engagement metrics carry the deck. The contracts flatten into a single line on a partnership slide. The argument becomes "users keep choosing this, and we have not yet started spending on growth."

The product did not change. The evidence configuration did, and the spine has to be reordered to match. Different verticals call for different narrative frameworks for pitch decks - same round, same product, different anchor.

Before drafting a slide, name which of the three spines applies. If the honest answer is "all three," the deck does not have a spine yet - it has three contradictory drafts in one file, and the investor will feel it. Borrowing the SaaS spine for a biotech deck is the most expensive narrative mistake in this category.

This is the second reason the article exists. Most storytelling advice argues for more story; some pitch contexts call for less. Three where story-led decks underperform:

If the audience already trusts the company or the data, story is overhead. Investor pitch storytelling is calibration, not maximisation. The default is to use a spine; the discipline is knowing when to compress it.

A practical control: re-read the deck and ask which slides exist to support the spine and which exist because every deck has that slide. Cut the latter. The companion question is structural - how many slides a deck needs at each stage. The strongest late-stage decks compress story to one or two slides; the strongest seed decks expand it across the spine. Same craft, opposite weighting.

These are storytelling-specific failure modes, not generic presentation mistakes. Four worth naming, each with a recovery move:

The first mistake is the most common and the easiest to fix. The fourth is the rarest and the hardest - by the time a deck has been over-engineered, the founder is too close to it to see the scaffolding, and the recovery is almost always a second reader.

Storytelling in a pitch deck supports a raise; it does not cause one. The strongest decks pair a story spine with stage-appropriate evidence and know when to compress one to make room for the other. The four decks each made the trade differently - Airbnb leaned hardest on story, Buffer on transparency, LinkedIn on category framing, Facebook on engagement data. None had to choose; all had to balance.

One souvenir before the deck opens: before writing a single slide, name the spine in one sentence and name which of the three vertical patterns it follows. If neither fits on one line, the deck does not have a spine yet.

If pressure-testing that spine is the work in front of you, the pitch deck design methodology we run at Whitepage Studio starts there.

Storytelling in a pitch deck is the underlying argument that gives every slide a reason to be in that order: the contradiction the company exists to resolve, the proof of motion that shows it can, and the stake explaining why it matters. It is not the slides - it is what the slides are evidence for. When investors recall a deck a week later, what they remember is the spine.

Pitch deck storytelling reduces friction. Investors review dozens of decks a week, and pure-data decks blur into each other; the deck with a narrative spine is the one that surfaces in the partner meeting on Monday. Motista research found emotional encoding roughly doubles spend across customer behaviour, and the same wiring applies to deck recall. Storytelling does not cause the raise; it supports it.

Start with the contradiction - the specific tension the company exists to resolve - and let every later slide carry evidence the gap is closable. Sequence the proof of motion and the stake around that spine. The cover slide should signal the company, not the founder. The story lives in the founder's head; the deck is the prop.

The strongest pitch deck story arc rests on three elements: contradiction, proof of motion, and stake. A three-act structure works; a ten-stage hero's journey does not. Decks that mirror screenplay frameworks read as performance, not investment. The Airbnb deck, with its rule-of-three rhythm across every load-bearing slide, is the cleanest public example of a narrative framework for pitch decks.

Investors care about both, in order. The numbers establish whether the meeting happens; the story decides whether the deck is remembered after it. Across 1,000+ decks at Whitepage Studio, the slides investors recall back to founders are story slides far more often than market-size slides. The weighting reverses at late stages.

867 BOYLSTON ST

BOSTON, MA 02116